Introduction

The checklist below details ten essential compliance tasks every Florida employer–sponsored 401(k) plan must address for the 2027 plan year.

1. Engage a qualified advisor or fiduciary partner

A qualified advisor earns their keep by turning a vague duty into a documented routine, so look for one that spells out the engagement before ever touching your plan. One provider’s 401k plan advisory services page, for example, breaks the work into clear stages: an upfront needs evaluation, a risk and cost assessment, an investment and participation review, and a comprehensive plan analysis, followed by hands-on implementation and ongoing benchmarking of investment performance and participation trends. That kind of stage-by-stage roadmap surfaces red-flag issues early and hands sponsors an audit-ready paper trail long before regulators ever knock.

Why it matters.

Regulators see you, not the payroll vendor or record-keeper, as the plan’s guardian. The Department of Labor is blunt: the sponsor is liable for every decision, dollar, and deadline.

That burden can overwhelm a Florida company already navigating hurricanes and seasonal hiring. Bringing in a dedicated 3 (16), 3 (21), or 3 (38) fiduciary off-loads day-to-day tasks (testing, filings, investment review) to professionals who live and breathe ERISA. The law calls this “monitoring fiduciary processes and decisions,” and outside experts excel at it.

The return is measurable: a sharp advisor tracks rule changes, builds an audit-ready paper trail, and flags problems early, protecting employee balances and your bottom line. In other words, the right partner turns compliance from a gamble into a reliable, repeatable system.

2. Update and align your plan document

Your plan document is the legal backbone of the entire 401(k). When it drifts outside current law, the plan’s tax-favored status is at risk, and the IRS knows it. The agency’s annual “checkup” starts with one question: “Has your plan document been updated within the past few years to reflect recent law changes?”

If “not sure” is your reply, trouble has already started. SECURE 2.0 alone rewrote dozens of provisions: auto-enrollment rules, higher catch-ups, emergency savings options, and the coming Saver’s Match. The IRS gave qualified 401(k) plans until December 31, 2026 to capture those changes in writing. Miss that date and the plan shifts from compliant to corrigible, triggering costly EPCRS filings or, worse, disqualification.

Block time this quarter with your advisor, record-keeper, or ERISA counsel. Pull the most recent restatement, each interim amendment, and the signed adoption agreement into one folder, digital or hard copy. Confirm three points:

Every mandatory change through SECURE 2.0 is drafted and signed.

Any optional features you’ve adopted (Roth match, emergency withdrawals, student-loan matching) are expressly permitted.

Day-to-day operations match the language on paper: eligibility rules, compensation definitions, vesting schedule.

If any box stays unchecked, draft the fix now while the remedial window remains open. The paperwork may look small, but it protects the plan from what the IRS calls its number-one audit finding. That’s peace of mind worth a brief document review.

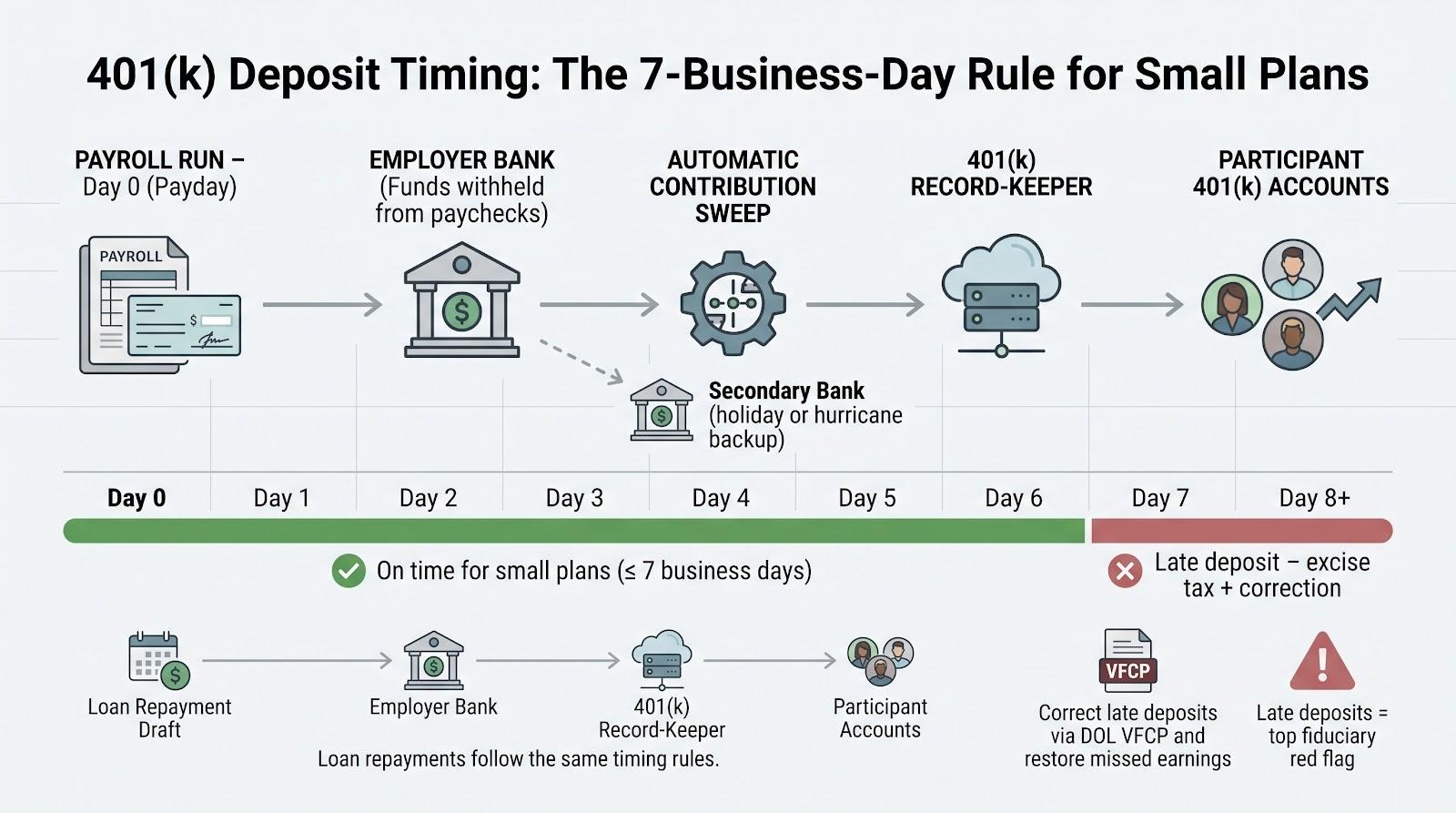

3. Move every paycheck dollar into the plan fast

When employees see money withheld on payday, they expect it to appear in their 401(k) right away. The law agrees. The Department of Labor requires deposits as soon as the funds can be segregated from corporate assets. For small plans, anything later than the seventh business day after payroll is automatically late.

Late deposits rank among the most common fiduciary missteps. Industry researchers call tardy contributions a top-tier “red flag,” one of the weaknesses found in more than eight in ten plans nationwide. Each violation can prompt a DOL audit, an excise tax of 15 percent on every delayed dollar, and required earnings make-ups paid by the employer (not the record-keeper).

The cure is operational. Link your payroll system to an automatic contribution sweep that runs every pay cycle. Reconcile the funding report the same day. If a holiday or hurricane stalls your primary bank, route cash through a secondary clearing account so money still reaches participant accounts on time. If a deposit slips, correct it at once and record the fix under the DOL’s Voluntary Fiduciary Correction Program. Regulators reward speed and clear documentation.

Loan repayments travel on the same rails. A missed loan draft can push a participant into default and convert the balance to taxable income. Handle loan money with the same urgency you give salary deferrals, and you remove one of the easiest ways to invite a fiduciary breach.

4. Pass (or quickly fix) your non-discrimination tests

Every qualified 401(k) must show that rank-and-file employees share the same advantages as owners and highly paid staff. Regulators enforce that fairness through three annual tests: ADP, ACP, and Top-Heavy. The IRS treats these tests as non-negotiable duties, right alongside fee reviews and notice deadlines.

For calendar-year plans, the clock starts the moment New Year’s confetti hits the floor. Census data goes to your TPA in January, test results arrive by February, and any failures must be corrected (refunds to highly compensated employees or QNEC contributions to everyone else) no later than March 15. Miss that date and an automatic 10 percent excise tax applies.

Failing a test is common; ignoring it is unforgivable. About 30 percent of small plans miss ADP or ACP each year, based on provider data. The good news: quick action restores compliance and soothes participants whose refunds show up in paychecks. Chronic failures, by contrast, signal design flaws, often low rank-and-file participation, that can draw audits or lawsuits.

How to stay on the right side of the line:

Push enrollment and match messages each fall so non-HCE deferrals rise before year-end.

If testing headaches persist, switch to a Safe Harbor design for 2028; it removes ADP and ACP testing in exchange for a fixed employer contribution.

Document every step: test reports, refund checks, and QNEC wires. Auditors first look for a paper trail that proves you spotted the issue and fixed it on time.

Treat these tests like a fire drill, fast, methodical, and fully logged, so your plan keeps its tax benefits and your team keeps saving without disruption.

5. Deliver every notice before the clock strikes midnight

A strong 401(k) earns trust by keeping participants informed. Federal rules back that principle with hard deadlines, and missing even one can erase key protections or trigger daily fines.

In practice, four annual notices carry most of the weight. Safe Harbor, QDIA, and Automatic Enrollment alerts set expectations for contributions and default investing. The 404a-5 fee disclosure tells employees what they pay and why. Many sponsors bundle all four, aiming to reach inboxes or mailboxes by December 1 for the coming plan year. Making December 1 your standing “notice day” removes calendar guesswork.

Adopt a checklist approach. Draft the notices, confirm addresses, then send through your record-keeper’s e-delivery system. Store the confirmation report with your plan files; auditors ask for proof.

Missed the window? You can still protect Safe Harbor status by switching to a nonelective 3 percent contribution and issuing a late notice within 30 days after plan year-end. The fix costs more than meeting the original deadline, so set safeguards such as calendar reminders, owner sign-offs, and provider alerts to keep everything on time.

Remember the event-based rules. Blackout periods longer than three days need a 30-day heads-up, and any mid-year amendment that reduces benefits requires prompt disclosure. When in doubt, communicate early and clearly. Timely notices keep employees engaged and regulators satisfied, two outcomes every Florida sponsor can celebrate.

6. File a clean Form 5500 and know when an audit follows

Official IRS Form 5500 first page for 401k annual reporting

Form 5500 is your plan’s annual report card. It lists every dollar of contributions, fees, and investment income in a filing that regulators and employees can view with one click. For calendar-year plans, the report is due July 31, 2027 (or October 15 with Form 5558). Miss the date and penalties can exceed $2,500 a day until the form is accepted, an avoidable hit to any Florida budget.

Accuracy matters as much as timing. Verify the plan name, EIN, participant counts, and characteristic codes before you press “submit” in EFAST2. Small typos invite follow-up letters, large ones invite field investigations. A quick review with your TPA or auditor keeps the form on track.

The audit trigger still surprises sponsors. A recent DOL rule says you now count only participants with an account balance on January 1. Reach 100 participants with balances and an independent CPA audit must accompany your 5500, unless the 80-to-120 transition rule applies. If you sit near the threshold, run the census early so you can reserve an auditor before spring calendars fill.

Treat the audit like a dress rehearsal for a future DOL exam. Auditors check payroll feeds, deposit timing, loan records, and investment oversight. The cleaner your files, the shorter and cheaper the engagement. Even if you stay under 100 lives, keep “audit-ready” books: reconcile contributions each pay period, archive notices, and store signed plan documents in one shareable folder.

Finish with a simple checklist: draft by May, finalize with partners in June, file in July (or extend), then save the stamped confirmation page with your plan binders. One disciplined workflow removes the costliest late-filing risk and shows, in writing, that your Florida team runs a tight ship.

7. Pressure-test your investments and fees every year

Plan participants trust you to curate smart, affordable funds. Plaintiff attorneys count on sponsors to forget. That gap keeps ERISA lawsuits in the headlines, which makes an annual investment checkup essential.

Start with performance. Pull one-, three-, and five-year numbers for every fund against its peer group. Flag any option that trails its benchmark or category median for two straight periods. Underperformance alone is not fatal, but you need a written reason to keep the fund, perhaps style drift is temporary or a manager change is underway. No reason? Replace the fund and record the decision.

Next, address fees. The DOL says expenses must be “reasonable” for the services delivered, so benchmark them. Compare expense ratios and record-keeping costs to at least three similar plans. If yours land in the top quartile, renegotiate or move. Courts have ruled that cheaper share classes of the same fund count as distinct options; ignoring them signals imprudence.

Document every step. Keep committee minutes that list the data reviewed, the questions asked, and the votes taken. Should litigation start, that paper trail proves a prudent process even if a fund later stumbles.

Finally, revisit your Investment Policy Statement. Does it still explain how you select, monitor, and replace funds? If not, revise it and obtain board approval. A clear IPS is both roadmap and first defense. Run this cycle each spring, share highlights with employees, and you will keep participants and regulators confident that their retirement dollars are in good hands.

8. Guard the piggy bank: bonding and cyber defense

Money lost to theft or hacking is gone forever unless you have the right safety nets. ERISA requires one of those nets: a fidelity bond equal to at least ten percent of plan assets (capped at $500,000, or $1 million if you hold company stock). A 2025 industry study found that 43 percent of plans nationwide carry regulatory red flags, with insufficient bond coverage among the four most severe. The fix costs a few hundred dollars a year, while the alternative can bankrupt a small employer forced to replace stolen assets.

Check your coverage amount every January. As the plan grows, the bond should rise with it. Keep the certificate on file, because auditors and the DOL ask for it first. If you discover a shortfall, call your broker and raise the limit the same day.

Next, address the growing threat of cyber-crime. Retirement accounts attract fraudsters, and the DOL now expects sponsors to vet provider security, require multi-factor authentication, and train staff to spot phishing. Build a routine: request SOC 1 and SOC 2 reports from your record-keeper each year, log any exceptions, and ask the vendor about patch timelines. Encourage participants to activate online access (dormant accounts invite fraud) and enable text alerts for withdrawals.

A right-sized bond paired with a living cybersecurity checklist can turn potential headlines into routine footnotes, protecting employee nest eggs and your company’s reputation.

9. Stay human: manage RMDs, hardships, loans, and lost accounts

Retirement money is personal. When a participant needs a hardship withdrawal or reaches age 73 and waits for an RMD, delays erode trust and may trigger IRS penalties. Handle these life-event transactions with concierge-level care.

Begin with RMDs. Each fall, pull an age report from your record-keeper. Anyone who turns 73 this year and is no longer on your payroll must receive a required minimum distribution by December 31 (first-timers may wait until April 1 next year, but a January payout doubles their tax hit). Set reminders, send letters, and follow up until every check clears.

Hardship requests deserve speed and empathy. SECURE 2.0 allows self-certification, so paperwork is lighter, yet you still need a process: receive the form, verify the amount, code the distribution, and issue the 1099-R. Keep each decision in a hardship log; auditors ask.

Loans run on autopilot until someone quits and repayments stop. Monitor payroll files each cycle. When a participant terminates, either set up ACH repayments or deem the loan default and issue tax reporting within 90 days. Clean loan ledgers keep Form 5500 errors, and angry former employees, off your plate.

Finally, search for missing participants before they become a headline. Once a year, cross-check returned mail, use free search engines, and contact beneficiaries. Document everything. If you truly cannot locate someone, consider rolling small balances to an IRA or reporting to the PBGC missing-participant registry. A proactive search shows regulators you value every dollar, even when the owner is silent.

10. Keep beneficiary designations and QDRO procedures current

A plan can run flawlessly on every deposit, test, and filing and still land in court over a single outdated beneficiary form. ERISA gives the named beneficiary on file the money, full stop, regardless of what a will or a family member expects. Sponsors who never revisit those forms are sitting on a dispute waiting to happen.

Build a yearly refresh into open enrollment. Remind every participant to confirm or update beneficiaries, especially after a marriage, divorce, birth, or death. Flag any account with no beneficiary on file at all; those defaults revert to a plan-document hierarchy that rarely matches what the employee would have chosen.

Divorce brings a second obligation: Qualified Domestic Relations Orders. When a court splits a participant's account between spouses, the plan needs written QDRO procedures already on file, not drafted in a scramble after the order lands on your desk. Route every incoming order to your TPA or ERISA counsel immediately, confirm it meets the plan's model-order format, and freeze the affected balance until the split is processed. A plan without a QDRO procedure risks paying the wrong party, a mistake that falls on the sponsor to fix.

Keep a simple log: participant name, last beneficiary update, and any QDRO on file. Ten minutes a quarter checking that log against new hires, terminations, and life events closes one of the easiest, and most overlooked, compliance gaps on this list.

Conclusion

Work through these ten items in order and Florida 401(k) compliance stops feeling like a guessing game. Each task protects plan assets, keeps regulators satisfied, and preserves the plan’s tax-favored status, while the documentation you build along the way becomes your best defense if the DOL or IRS ever calls. Tackle the checklist early in the plan year, log every step, and your employees can stay focused on what matters most: saving for retirement without costly surprises.