6 Best Small Business Loans for Property Management Companies in 2026

Interest rates are still perched near their cycle highs, and banks keep tightening standards, according to the Federal Reserve’s Senior Loan Officer Survey (KPMG). Yet small firms drew a record $56 billion in SBA-backed funding last fiscal year—a 7 percent jump, according to the Associated Press.

If you manage properties, you feel both forces every day: growth opportunities keep knocking while capital costs more and moves slower. We tested dozens of financing products and narrowed the field to six that balance price, speed, and real-world fit for repairs, renovations, and acquisitions in 2026. Keep reading to see which one earns your next application.

How we selected and scored each loan

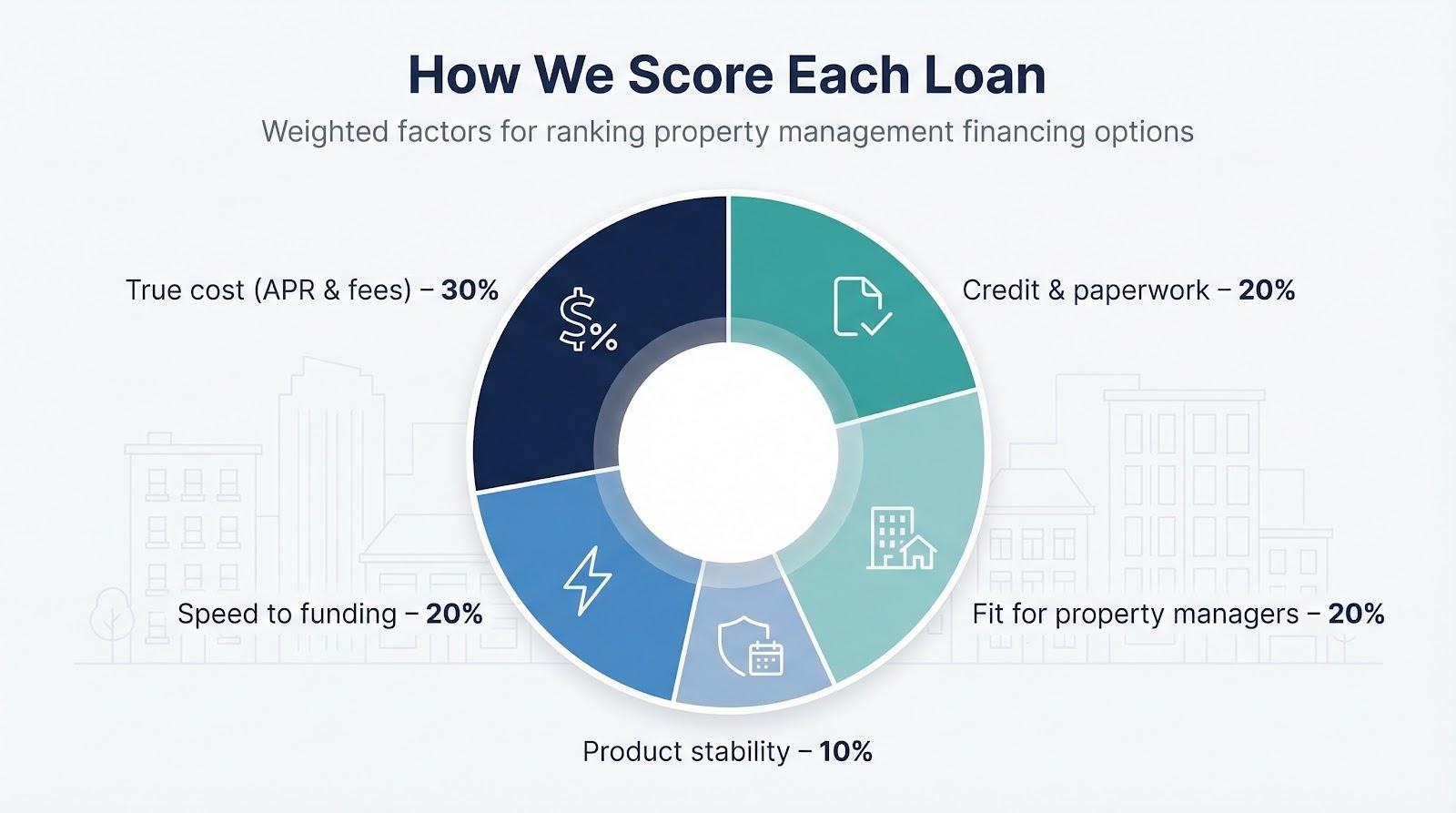

Before handing you a ranked lineup, we put every loan through the same five-factor test. We asked:

What does the money truly cost once fees and interest settle in?

How tough is the credit and paperwork hurdle?

How quickly can funds land in your operating account?

Does the structure fit a property manager’s world, including big-ticket upgrades, recurring repairs, and unpredictable cash gaps?

Will this product still be on the shelf next quarter?

We weighted those questions 30-20-20-20-10 percent in that order, then converted raw data (APR ranges, approval rates, average days to funding) into a 100-point score.

That scoring system compares apples to apples. It penalizes expensive cash advances, rewards low-rate SBA terms, and keeps speed in the spotlight for emergencies. The result is a list you can trust because every pick earned its place on measurable merits, not marketing hype.

The 6 best small-business loan options (ranked)

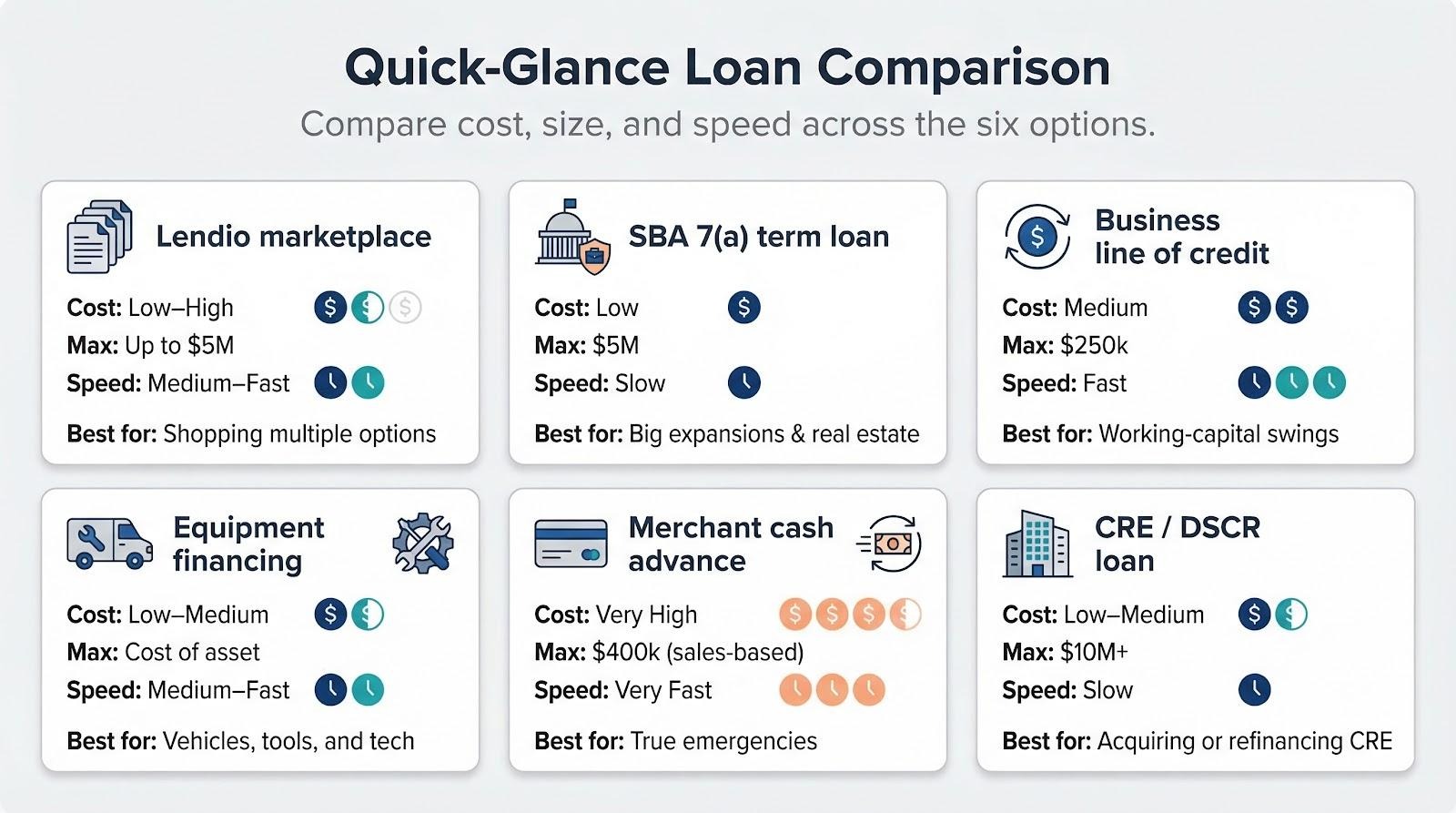

1. Lendio: best one-stop marketplace

Think of Lendio as the Trivago of business lending. Start by estimating payments with Lendio free loan calculators, then submit one short application so the platform can scan more than 75 banks, credit unions, and fintech lenders and show tailored offers side by side. That single step saves you days of duplicate paperwork and follow-up calls.

For a property-management firm, that breadth pays off in two ways. First, you see different term-loan, line-of-credit, and SBA quotes in the same dashboard, so it becomes obvious which structure keeps cash flow smoothest when roofs leak in February. Second, the algorithm does not dismiss a mid-600 credit score; it simply matches you with lenders who accept that profile.

Lendio never charges a brokerage fee. Your cost depends on the offer you accept: SBA terms can start near single digits, while fast-cash products cost more. Funding usually lands within a week of choosing a lender. The wide menu and low friction earn Lendio the top spot.

2. SBA 7(a) loan: best for big-ticket expansion

When you need seven figures to buy an apartment building or modernize a complex, the SBA 7(a) program is the heavyweight choice. The government guarantees up to 85 percent of the balance, letting banks stretch repayment to 25 years and keep rates in the low double digits despite recent hikes.

That affordability can transform your budget. Long terms shrink the monthly payment to a level your rent roll can handle. You can often finance up to 90 percent of the purchase price, so a modest down payment unlocks a large asset.

Qualifying takes patience. Lenders expect at least two profitable years, a mid-650 FICO, and statements showing the property will cash-flow after debt service. Underwriting runs weeks, and you must pledge the real estate and sign a personal guarantee.

The payoff for that paperwork marathon is the lowest long-term cost on this list. If your books are clean and your growth plan is bold, the 7(a) loan offers the most economical fuel.

3. Business line of credit: best for working-capital breathing room

Every property manager knows lumpy cash flow. One month rent arrives on time; the next you front thousands for an HVAC overhaul. A revolving business line of credit handles that roller-coaster.

The lender sets a ceiling—often $5 000 to $250 000—based on revenue and credit. You draw only what you need, pay interest on the outstanding balance, then reuse the line after you repay. Online providers such as Bluevine streamline the process: firms with $120 000 in annual revenue and personal scores in the low 600s can finish the application over lunch. Approvals often arrive within a day, and funds can post the next morning. Rates start in the high single digits for prime borrowers and rise with risk, but flexibility is the draw: borrow for payroll on Monday, repay after Friday rent, and skip prepayment penalties.

That agility earns the line of credit third place. It will not fund a building purchase, yet nothing beats it for smoothing day-to-day swings and keeping vendors paid without dipping into personal reserves.

4. Equipment financing: best for vehicles, tools, and tech

Service vans, zero-turn mowers, security cameras, even cloud-based software—equipment powers a property-management operation. Buying it outright strains cash, while leasing forever sacrifices equity. Equipment financing lands in the middle.

The asset secures its own loan. Lenders cover up to 100 percent of the purchase price, you repay over three to seven years, and the gear serves as collateral. Because the bank can repossess that backhoe if payments stop, rates often sit below unsecured loans, usually mid-single to low-teens even in today’s climate.

Documentation is light. Provide a quote or invoice, recent bank statements, and a personal score around 600, and many specialty lenders can approve within 48 hours. Speed keeps projects moving; no waiting months to replace a failing boiler while tenants shiver.

The trade-off is focus. Funds must buy the named equipment, nothing more. You also carry the risk that the asset loses value faster than the loan balance, a concern for tech that ages quickly. Still, when you need wheels, lifts, or servers now and prefer to own, equipment financing balances affordability and control.

5. Merchant cash advance and invoice factoring: best for lightning-fast, last-resort cash

Emergencies ignore calendars. A main water line bursts, or a roof collapses after ice, and you need five figures wired yesterday. When traditional underwriting would take weeks you do not have, merchant cash advances (MCAs) and invoice factoring unlock funds quickly.

With an MCA, a funder provides a lump sum in exchange for a slice of future card receipts. Payback happens automatically each day you process tenant fees or ancillary income, so personal credit matters less. Approval can land within hours, and many providers fund within 24 to 48 hours.

Factoring follows the same speed principle but taps receivables instead of card sales. You sell an unpaid invoice at a discount—usually 70 to 90 percent upfront—then forward the remaining balance, minus the fee, when the client pays.

Speed and leniency cost plenty. MCA factor rates often translate to effective APRs north of 50 percent. Factoring fees can run 1 to 5 percent for every 30 days the invoice stays open. If cash flow is thin, those deductions bite hard.

That is why these products rank fifth. They solve true crises; treat them like a fire extinguisher, use briefly, and refinance into cheaper debt once the emergency ends.

6. Commercial real-estate and DSCR loans: best for acquiring or refinancing income property

When your management firm owns bricks and mortar, a standard business loan rarely stretches far enough. Commercial real-estate (CRE) mortgages and debt-service-coverage-ratio (DSCR) loans suit million-dollar purchases and long-term holds.

Both underwrite the building first and you second. Lenders focus on net operating income and expect a DSCR of about 1.25:1—rent must cover projected debt payments with a 25 percent cushion. Meet that mark and you can borrow well past $5 million with repayment terms up to 30 years.

As of early 2026, strong-credit borrowers are locking fixed rates in the high-six to mid-nine percent range, a bargain compared with unsecured financing of equal size. Because the building secures the note, lenders can stretch amortization, which keeps monthly payments gentle even at today’s elevated rates.

Down payments usually run 20 to 30 percent, and closing resembles a residential mortgage on steroids: appraisals, environmental reviews, and full legal checks. Plan on six to eight weeks from term sheet to funding.

We rank CRE and DSCR loans sixth because qualification is exacting and the process slow, but no other option delivers such patient, comparatively low-cost capital for a multi-million-dollar asset.

Quick-glance loan comparison

You have met the contenders one by one. Now let us set them side by side so you can spot the right fit at a glance.

Loan type | Typical maximum | Rate range (APR) | Term length | Minimum credit | Collateral | Primary use |

Lendio marketplace (various) | Up to $5 million | Five to 40 percent | Six months to 25 years | 560+ | Varies by offer | Any; shop multiple options |

SBA 7(a) term loan | $5 million | Around 10 percent | Up to 25 years | 650+ | Business assets and personal guarantee | Large expansions, real estate |

Business line of credit | $250 000 | Seven to 30 percent | Revolving, six to 12 months | 600+ | Usually none | Working-capital swings |

Equipment financing | Cost of asset | Six to 15 percent | Three to seven years | 600+ | The equipment | Vehicles, tools, tech |

Merchant cash advance | $400 000 (sales based) | Effective APR of 50 percent or higher | Three to 18 months | 500+ | Future card sales | Emergency cash |

CRE / DSCR loan | $10 million+ | 6.5 to 9.5 percent | 15 to 30 years | 650+ | Subject property | Acquire or refinance CRE |

How to choose the right loan

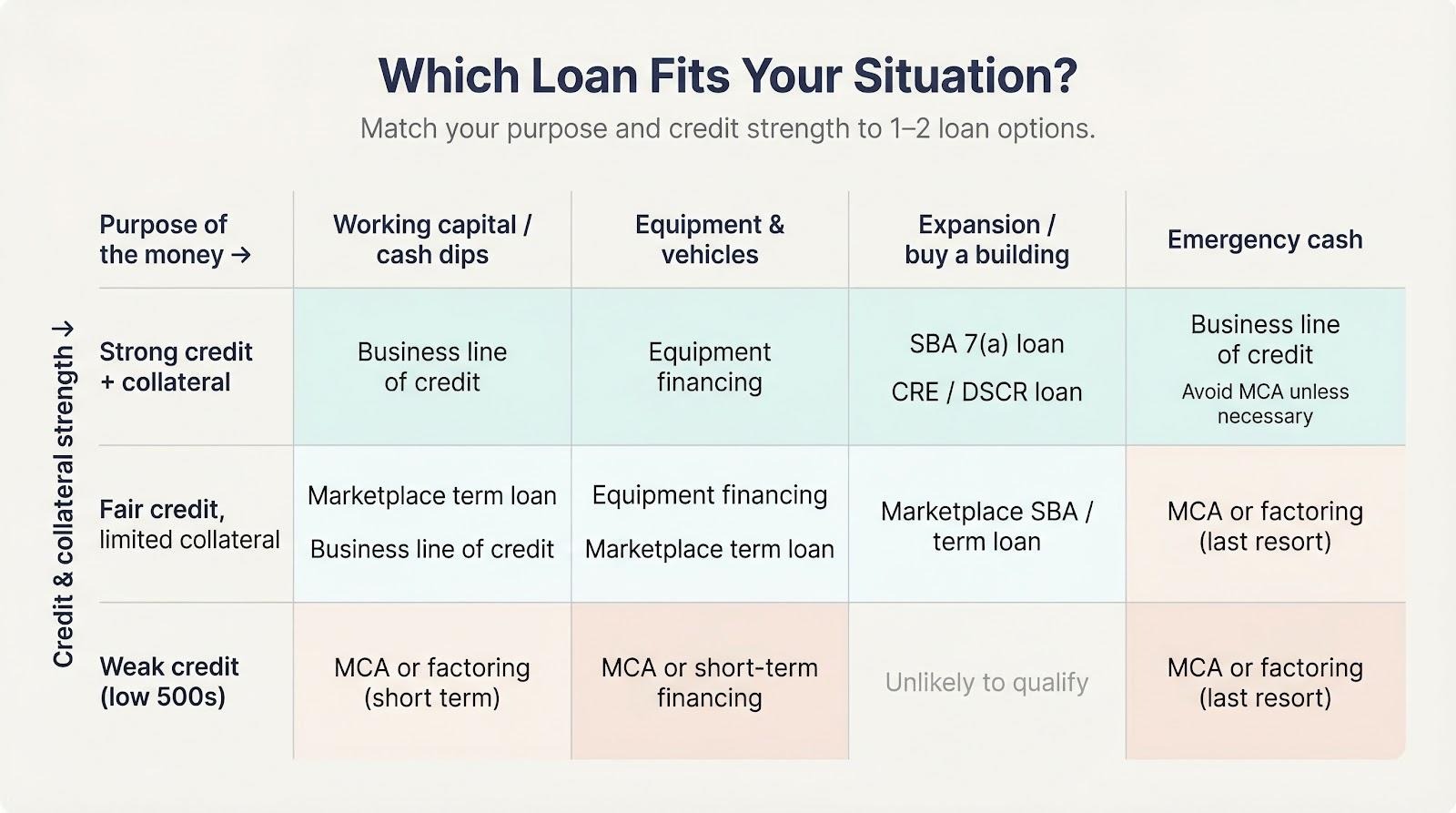

Even the best menu helps only if you know what to order. Let’s use a simple two-step filter to sort the six loans into clear yes-or-no buckets.

First, define what the money must accomplish. Are you expanding, buying a building, installing solar, replacing a fleet of trucks, or smoothing everyday cash dips? Expansion needs long, affordable capital, so start with an SBA 7(a) or a CRE / DSCR loan. Day-to-day swings call for speed and flexibility, so a revolving line, or in a true emergency an MCA, fits the bill.

Second, review your current strength: credit score, collateral, and time in business. Strong credit plus collateral opens the lowest-cost tiers of SBA or CRE financing. Fair credit but little collateral points toward a marketplace term loan or equipment financing. Scores in the low 500s leave only MCAs or factoring, and those should stay short term.

Picture a simple grid. Purpose runs left to right, credit strength top to bottom. Where they cross, one or two products stand out. Plug the rates from our table into a payment calculator and you’ll see the monthly impact in black and white. Decision made.

Conclusion and application tips for property-management companies

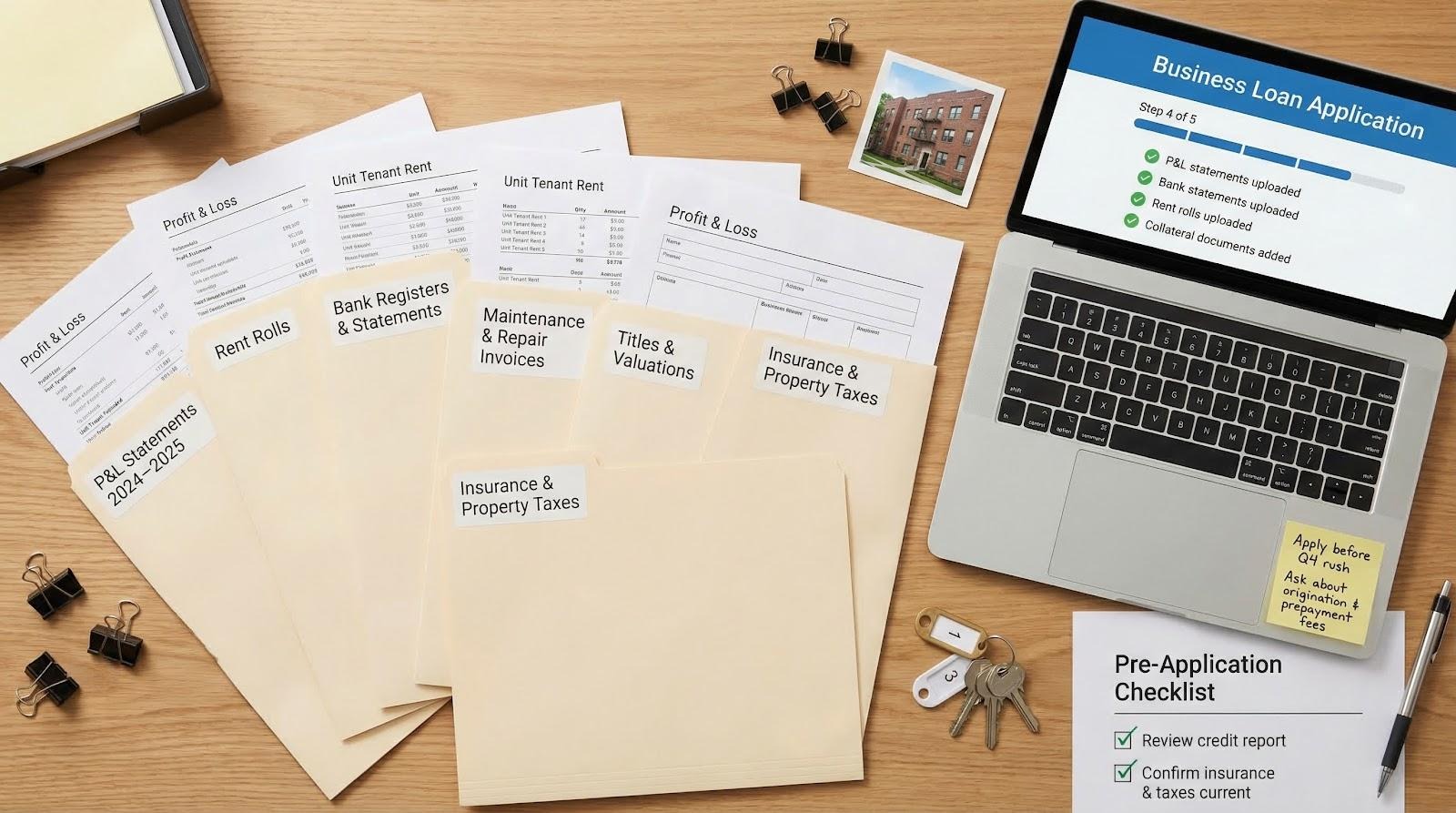

Lenders like tidy books. Before you click “apply,” pull the last two years of profit-and-loss statements, bank registers, and rent rolls into one folder. Add photos or invoices for any repairs you postponed until funding arrives. That packet shows underwriters you run an organized ship, which shortens review time and strengthens your bargaining hand.

Credit still matters, and you control more of it than you think. Pay personal cards below 30 percent utilization, fix reporting errors, and keep vendor accounts current. A 20-point jump in your FICO can shave whole percentage points off the final rate.

Gather original titles and a recent valuation when you plan to pledge vehicles or equipment so the lender does not spend a week hunting them. For real-estate deals, update insurance certificates and confirm property taxes are paid.

Timing counts. Bank and SBA pipelines swell in the fourth quarter as owners rush to close books; start earlier in the year when possible. Rates often dip when markets expect a Fed pause, so watch policy meetings and lock a term sheet quickly when the window opens.

Negotiate more than the interest line. Ask about origination fees, monthly maintenance charges on credit lines, and prepayment penalties. Lenders frequently trim those edges to win your signature, and the savings add up long after the headline APR fades from memory.